The biggest misconception about property ownership hit me hard when I started investigating property title fraud cases. Homeowners believe recording a deed creates a protective barrier around their property—but property title fraud exploits exactly this assumption.

The reality is far more unsettling.

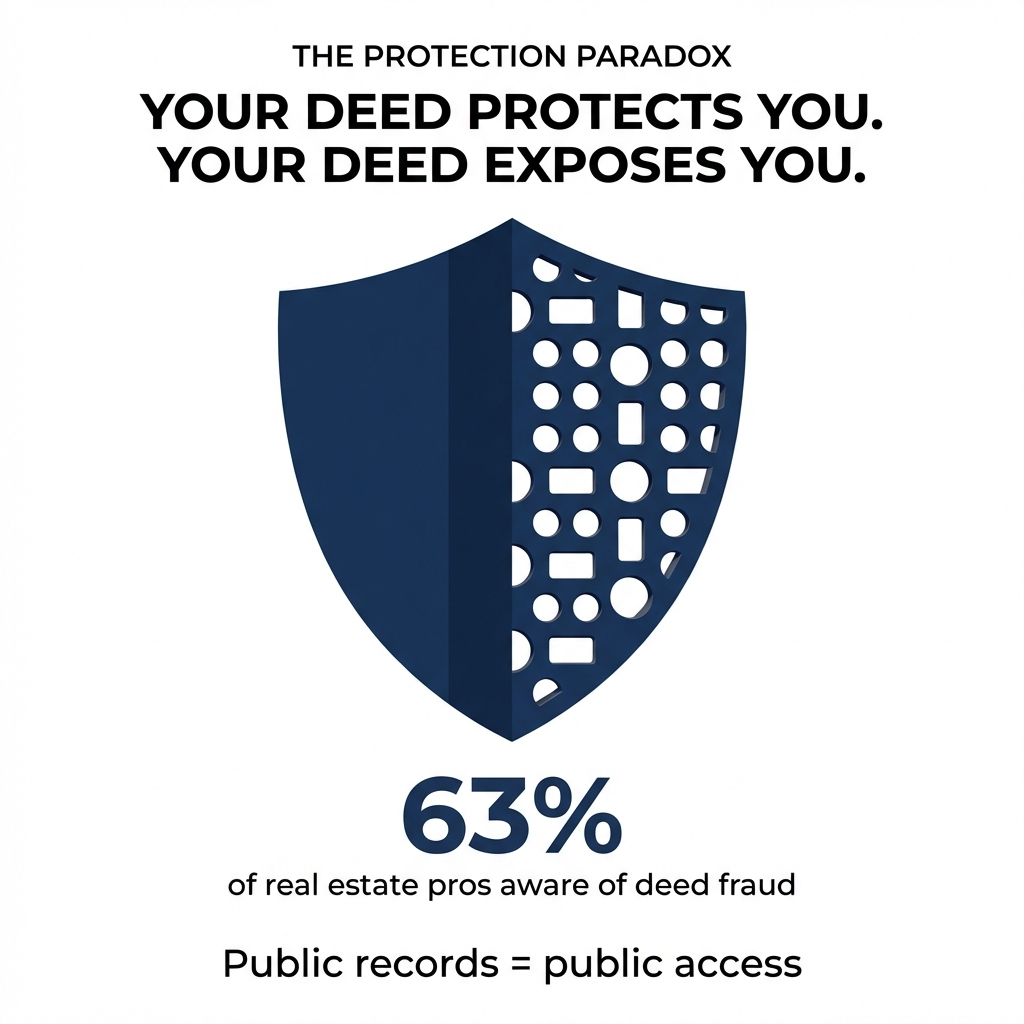

The public record system designed to protect you is the same system making you vulnerable.

I’ve watched this pattern repeat across the country. According to the National Association of REALTORS®, 63% of real estate professionals reported awareness of deed fraud in their markets within the past 12 months. In the Northeast, that number jumps to 92%.

This isn’t theoretical. Between 2019 and 2023, the FBI documented 58,141 victims who lost $1.3 billion to real estate fraud.

How Property Title Fraud Works Against You

Anyone can walk into a county recorder’s office or go online and access your complete property information. Your name, address, purchase price, acquisition date, even your signature from the deed are all publicly available.

Criminals use this information to forge documents and file fraudulent deeds.

The county recorder’s office isn’t verifying the authenticity of the person filing. They’re just checking that the paperwork is filled out correctly.

A fraudster can steal your property on paper by filing a fake deed that transfers ownership to themselves or a shell company. The system accepts it because it looks legitimate.

By the time you discover the fraud, they’ve often taken out loans against your property or sold it to an unsuspecting buyer.

The Clerical Review Problem

The recorder’s office performs a clerical review, not a security review. They verify:

- The legal description is correct

- The document is notarized

- Formatting requirements are met

- Signatures are present

- The filing fee is paid

What they don’t do reveals the vulnerability:

- They don’t verify the person filing is actually the property owner

- They don’t call you to confirm you intended to transfer your property

- They don’t compare signatures between the new deed and your original deed

- They don’t require the actual property owner to appear in person with government ID

Even notarization doesn’t solve this. Notaries can be complicit in the fraud, or fraudsters can use fake IDs to get documents notarized.

I’ve seen cases where someone showed up with a driver’s license that had the real owner’s name but the fraudster’s photo. The notary checked the box. The recorder accepted the document. The property was stolen.

The system assumes good faith. It’s built for efficiency and public access, not security.

A Case That Changed My Perspective

A Florida case opened my eyes to how brazen these schemes have become.

An elderly woman owned her home outright. Paid off. Worth about $400,000. She still lived there, was mentally sharp, managed her own affairs.

A fraudster obtained her personal information and created a fake ID with her name and an accomplice’s photo.

They found a notary who didn’t look closely. They filed a deed transferring the property to an LLC they’d set up the week before.

The entire scheme took three days.

Three days from filing the fraudulent deed to securing a $300,000 home equity line of credit against her property.

The lender did a title search, saw the recent deed transfer to the LLC, verified the LLC existed, and approved the loan.

The fraudsters got the money wired and disappeared.

The woman discovered the fraud six weeks later when the lender sent a payment notice to the property. By then, the money was gone, laundered through multiple accounts.

The system worked perfectly at every step. The recorder recorded. The notary notarized. The lender lent.

But nobody ever contacted the actual human being who owned the home.

She was erased on paper while still living in her own house.

Who Gets Targeted by Property Title Fraud

The data reveals a troubling pattern. According to NAR’s 2025 survey, only 12% of title fraud cases involved owner-occupied homes. Meanwhile, 62% involved vacant land.

Vacant properties are five times more vulnerable than owner-occupied homes.

Fraudsters target properties where owners are less likely to notice suspicious activity immediately.

Seniors face disproportionate losses. While people 60 and older represented only 19% of complaints, they lost almost 44% of the money totaling $76.3 million.

Criminals deliberately target older homeowners because they often have substantial equity and may not monitor their credit or property records daily.

The Parcel ID Paradox

Each separate parcel or lot has a unique identification number. This system allows for orderly distribution of property taxes, assessments, and municipal improvements.

The ID number identifies boundaries when property ownership transfers to ensure clear title and prevent future ownership disputes.

But here’s what most people miss about parcel IDs.

The same system that protects your property can expose you to risk. When you combine two adjoining parcels into one, you might save money on certain fees or simplify your tax situation.

You might also create a security gap.

Consolidating parcels requires filing new documents with the county. This process creates a paper trail that fraudsters monitor.

The consolidation itself isn’t the vulnerability. The vulnerability is in the public record of the change, which signals to criminals that you’re actively managing the property and may not be closely monitoring for unusual activity during the transition period.

I’ve seen cases where fraudsters specifically targeted properties that recently underwent parcel consolidation. They filed fraudulent deeds during the administrative window when the county was still processing the legitimate consolidation paperwork.

The Title Insurance Gap

A qualified real estate closing attorney can conduct proper title searches that help detect property title fraud before it costs you your home.

Most homeowners assume their title insurance protects them from deed fraud.

It doesn’t work the way you think.

Title insurance protects against defects in title that existed before you purchased the property. It doesn’t protect against fraud that occurs after you own the property.

If someone files a fraudulent deed transferring your property after you’ve owned it for years, your title insurance policy likely won’t cover it.

Owner’s title insurance may help with legal costs to fight fraudulent claims, but even then, you’re facing months or years of legal battles to reclaim your property.

The forged deed may be legally void, but the practical reality is substantial financial and emotional tolls.

Three Steps to Protect Against Property Title Fraud

1. Sign up for property alert systems

Electronic notification systems alert property owners when documents are filed. These systems exist in 14 states: Arizona, California, Florida, Georgia, Illinois, Indiana, Maryland, Massachusetts, Nevada, Ohio, Pennsylvania, South Carolina, Tennessee, and Washington.

Check if your county offers free property monitoring. Sign up immediately. You’ll receive alerts within 24 to 48 hours when any document is recorded against your property.

2. Monitor your credit and property records quarterly

Pull your credit report every three months. Look for new loans or lines of credit you didn’t open.

Search your property address in your county’s online property records system. Verify no unexpected deeds or liens have been filed.

Set calendar reminders. Make this routine.

3. Consider deed fraud insurance

Some insurers now offer specific deed fraud coverage separate from traditional title insurance. This coverage typically costs $100 to $300 annually and covers legal expenses to fight fraudulent transfers.

Read the policy carefully. Verify it covers fraud that occurs after you purchase the property, not just pre-existing title defects.

What’s Changing

Some jurisdictions are responding. Franklin County, Ohio created a Deed Fraud Strike Force in 2024. Virginia conducted a comprehensive study identifying red flags like remote notarization requests and below-market pricing.

The FBI Boston Division issued specific warnings about quit claim deed fraud in April 2025, noting a steady increase in reports.

But legislative and technological responses are inconsistent across jurisdictions. The fundamental vulnerability remains: county recorders process approximately 50,000 home titles every year with fewer than 10 deeds flagged as potentially fraudulent.

That low detection rate doesn’t mean fraud is rare. It means most fraudulent deeds pass through the system undetected because recorders lack the authority and tools to verify authenticity.

The Real Threat: Property Title Fraud Is Growing

The vulnerability isn’t in the recording system failing. It’s in the system working exactly as designed, but with no real identity verification built in.

The system assumes good faith. It connects paperwork to paperwork, not paperwork to people.

Until that fundamental design changes, property owners need to become their own first line of defense.

Monitor your property records. Sign up for alerts. Understand that your deed recording doesn’t create a protective barrier.

It creates a public record that criminals can exploit.

The question isn’t whether deed fraud will continue. The question is whether you’ll discover it before the damage becomes irreversible.