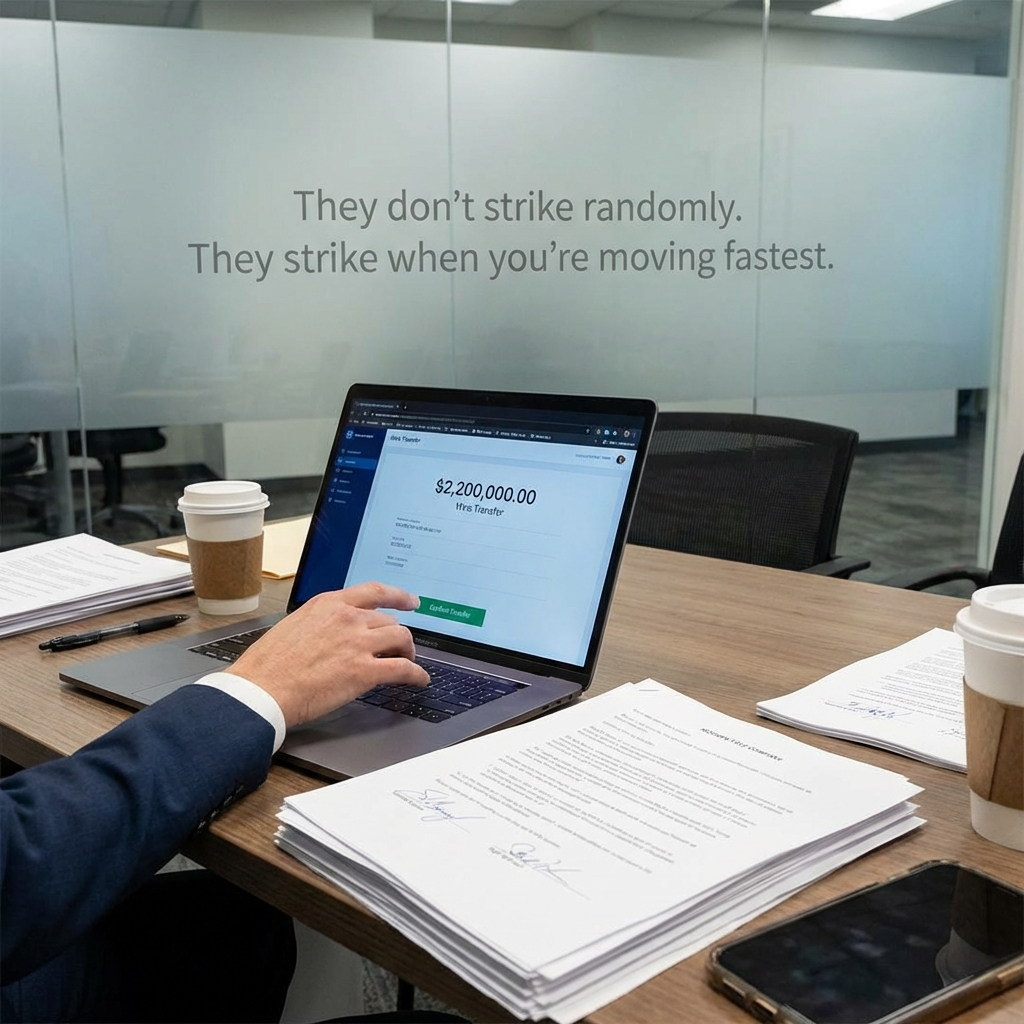

Johanna Berkowitz lost $2.2 million in seconds—a victim of real estate wire fraud that started with a single compromised email.

An email arrived. It looked legitimate. It came from what appeared to be her attorney’s address. The instructions were clear: wire the funds to finalize the closing. She did what any reasonable person would do. She followed the instructions.

The money vanished into a fraudulent account controlled by criminals who had been watching her transaction unfold for weeks.

When I first heard about this case, my reaction wasn’t shock. It was recognition. This could happen to anyone. Title transfer frauds are more common than most people realize. The gap between what’s actually happening and what people think is happening grows wider every day.

Real Estate Wire Fraud: The Hidden Epidemic

Real estate wire fraud losses exploded from $9 million in 2015 to $446 million by 2022. That’s a fiftyfold increase in less than a decade.

By 2024, these scams accounted for an estimated $500 million of the $12.5 billion in total cybercrime losses. But here’s what keeps me up at night: only 59% of title companies report fraud incidents to authorities. The true scale is significantly higher than official numbers show.

Nearly one in four consumers received suspicious communications during their real estate closing. Of those targeted, one in 20 became a victim. The median loss exceeds $70,000. That’s often a family’s entire life savings.

Why Your Data Is More Vulnerable Than You Think

Property and client data isn’t as protected as it should be. Buying a house involves 6-7 stakeholders, mostly unorganized and small business operators. You send your personal information to realtors for verification. You share it with multiple brokerages when shopping for interest rates. Home appraisers receive it. Lawyers receive it.

The data travels through emails. Through WhatsApp messages. Through systems that were never designed to protect information worth millions of dollars.

In a typical real estate transaction, up to 12 parties exchange information using disconnected systems. Each handoff creates an opportunity for criminals to intercept communications. The fragmented nature of the industry makes data protection nearly impossible.

The Critical Vulnerability Window

Working with a trusted real estate closing attorney who uses verified secure channels significantly reduces your exposure to real estate wire fraud.

Fraudsters don’t just randomly target people. They time their attacks with surgical precision.

They intercept communications and monitor email exchanges between parties for days, sometimes weeks. They wait for discussions about closing costs and wire transfers. Then they strike right before closing, when everyone is moving quickly and least likely to slow down to verify.

22% of fraudulent communications appear to come from the victim’s real estate agent. The criminals exploit the trust relationship at the heart of every transaction.

In one Connecticut case documented by the FBI, a buyer received a spoofed email from their supposed attorney instructing them to wire $426,000 to finalize the closing. This came two days after receiving legitimate preliminary communication from the actual title company. The timing wasn’t accidental.

The Accountability Gap Nobody Talks About

An American Land Title Association survey found that 17% of title companies sent money to an incorrect account last year. Of those, half did so more than once.

This reveals a systemic failure in verification protocols across the industry.

Meanwhile, 51.8% of real estate transactions in the last quarter of 2023 contained risk indicators for wire or title fraud. That’s an all-time high. The industry’s reactive approach has created an environment where fraudsters exploit gaps between banks, title companies, and real estate firms with little resistance.

Why Recovery Isn’t the Answer to Real Estate Wire Fraud

Johanna Berkowitz’s lawsuit seeks to subpoena IP addresses and banking records to recover her stolen money. The FBI’s Recovery Asset Team successfully placed holds on $538.39 million of fraudulent wire transfers in 2023, achieving a 71% success rate.

But that represents only a fraction of total losses.

Funds sent to domestic fraudulent accounts are often depleted rapidly through cash withdrawals or transferred to secondary accounts. What makes recovery even more challenging is that 22% of victims choose not to report the crime at all.

Prevention must beat recovery as the industry standard. Waiting until after the money disappears is too late.

What Could Have Stopped This Real Estate Wire Fraud

The Berkowitz case didn’t have to happen. Specific security protocols could have prevented this $2.2 million loss.

Verification protocols that require voice confirmation before any wire transfer. Multi-factor authentication for all parties in the transaction. Encrypted communication channels instead of standard email. Real-time monitoring systems that flag sudden changes in wiring instructions.

The technology exists. The protocols exist. What’s missing is the will to make them mandatory across every real estate transaction.

The Future We Need

Consumer data protection must be embedded in every step of the real estate process. This can’t be optional. It can’t be something you hope your title company takes seriously.

The $12.5 billion fraud epidemic isn’t inevitable. It’s the result of accepting fragmented systems, unverified communications, and reactive security measures as normal.

Johanna Berkowitz’s story should be the last of its kind. But it won’t be until we stop treating data security as someone else’s problem and start demanding it as the baseline standard for every real estate transaction.

Your life savings deserve better than an email and a prayer.